ATO appeals to High Court after reversal of PepsiCo decision

30/08/2024

The ATO has sought special leave to appeal to the High Court, following the decision in Full Federal Court (by a 2 – 1 majority) in PepsiCo, Inc v Commissioner of Taxation [2024] FCAFC 86, which overturned the single decision that ruled in favour of the Commissioner’s position.

The High Court decision when released, is significant to Multinationals with commercial arrangements with third parties, given the ATO’s focus on royalties and intangibles arrangements and its position on ‘embedded royalties’. Furthermore, this is the first case to consider the application of Diverted Profit Tax (DPT), a punitive tax of 40% targeting Multinationals engaging in artificial arrangements to transfer profits offshore.

While the majority found that payments under the two exclusive bottling agreements (EBAs) were between arm’s length parties and not royalties, all three judges agreed that even if the payments were for use of intellectual property (IP), the amounts ‘did not come home’ to Pepsico. This was because the nominated related entity supplying the concentrate is the creditor that SAPL (as a debtor) owed the obligation, not PepsiCo. The majority also determined that as the payments did not comprise of a royalty component, DPT, being the second issue considered, would not have applied to the arrangement.

In its media release, the ATO has indicated practical guidance is being developed for publication in late 2024 to illustrate its view as set out in the draft ruling.

Besides seeking special leave, the ATO also announced deferring the finalisation of draft ruling TR 2024/D1 (discussed here), relating to character of payments under software arrangement pending the outcome of the High Court proceeding.

Key findings

Regardless of the outcome from the special leave application and given the lack of unanimous decisions, there is little doubt scrutinising intangible arrangements by the ATO to identify any ‘embedded’ royalties is here to stay.

It is evident that the way a commercial agreement is being drafted is critical, from both the FFC’s majority and minority judgements, which ultimately can still be interpreted differently. Nevertheless, the Court has focused on the contractual terms of EBAs, with the majority substantially emphasising that the parties were dealing at arm’s length and engaged in extensive bargaining which resulted in the terms of the EBAs.

The Court also expects the Commissioner and taxpayers when putting forward their position, providing qualitative and quantitative evidence to support the economic and commercial substance of the arrangement.

Background

In summary, the relevant facts of the case are as follow:

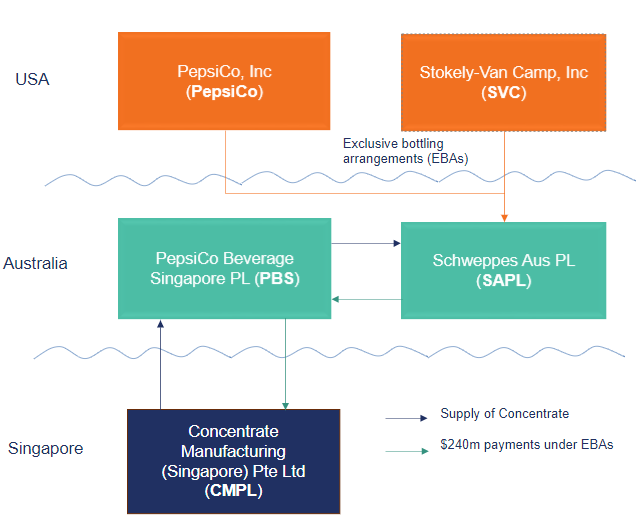

- PepsiCo and Stokely-Van Camp (SVC) are both US tax residents and the respective owners to a portfolio of trademarks and designs to the Pepsi and Gatorade brands.

- The companies entered into separate EBAs with Schweppes Australia Pty Limited (SAPL) to manufacture, bottle and package beverages in the Pepsi/Gatorade brands.

- The EBAs expressively stipulated that SAPL would only pay for the concentrate and did not explicitly provide for any payment of royalty for the right to use the relevant IPs. However, the EBAs implicitly and explicitly allowed the use of the relevant trademarks and intellectual properties.

- Under the EBAs, SAPL would purchase beverage concentrate from PepsiCo/SVC (or a related entity) according to formulas, specifications, etc provided to produce drinks for retail sale. From January 2018, such concentrate was purchased from a nominated Singapore entity CMPL through PBS, an Australian subsidiary of PepsiCo.

- As there were no royalties under the EBAs, no withholding tax was paid in Australia.

The Commissioner contended that:

- Royalties were ‘embedded’ within the payments made by SAPL and subjected to Article 12 of the United States – Australia Double Tax Agreement. Accordingly, PepsiCo and SVC were liable for royalty withholding tax (RWHT) under s128B of the Income Tax Assessment Act 1936 of $3.6m.

- Alternatively, one of the principal purposes in carrying out the scheme was to obtain a tax benefit (i.e. not liable for RWHT) such that DPT would apply. In this scenario, the tax liability pursuant under Part IVA would be $28.9m.

Federal Court – single judge

During the trial, Justice Moshinsky concluded that:

- RWHT was payable on the implied use of PepsiCo’s trademarks and IP, otherwise SAPL would be unable able to package and sell beverages under PepsiCo’s and SVC’s brands. It also would not have made any payments if not for the use of IP.

- The nomination of PBS as a seller of the concentrate constituted a direction to pay, but PepsiCo/SVC remained beneficially entitled for the purposes of Article 12 of the US DTA

- DPT provisions would apply in the alternative position as PepsiCo/SVC obtained a tax benefit by not being liable to Australian RWHT and reducing their US tax on income. This arose from the disconnect between the legal form and economic substance of the EBAs, where payments covered concentrate and licence of trademarks. and other IPs.

Full Federal Court decision

First issue

The majority (Justice Perram and Jackman) rejected the Commissioner’s argument (i.e. no royalties) on the basis that:

- The EBAs were commercially negotiated contracts between third parties and there was no dispute as to the reasonableness of the contracts.

- The Commissioner oversimplified the arrangement that only SAPL benefited from the granting of the licence and ignored any restrictions placed on SAPL’s entitlement to use the trademarks and other IPs (i.e only using the trademarks for the purpose of selling the beverages and nothing else).

- The licence for the use of trademarks and other intellectual properties were not granted to SAPL for free, as the rights did not exist in insolation. Instead, such rights were intertwined with SAPL’s obligations to distribute the beverages.

- There was no payment on direction since there was no antecedent monetary obligation owed by PepsiCo/SVC. As a related entity (i.e. PBS) was nominated as the seller in the EBAs, it was clear that PepsiCo/SVC would not be selling the concentrate and only contractually bound to ensure the quality of concentrate supplied.

Justice Colvin in dissent, made the following observations:

- Consideration stated in an agreement may not be required to separate into components corresponding different aspects because there was no commercial need to do so. Similarly, an amount calculated based on reference to pricing per unit of product supplied does not necessarily mean consideration is only paid for that product and nothing else. Circumstances known to the parties could resolve the ambiguity.

- The EBAs were between PepsiCo/SVC and SAPL and should SAPL fail to purchase and/or pay under the agreements, PepsiCo would be the entity suing the breach, not the nominee.

- The EBAs were properly construed as agreements to bottle, sell and distribute branded products, not agreements for the supply of concentrate. Accordingly, the payments made were partly in consideration for the use of trademarks which SAPL was licensed to use and supported the notion of an embedded royalty.

- After PepsiCo nominated a related entity as the seller and the Nominee supplied the concentrate, PepsiCo/SVC no longer had beneficial entitlement to the income and thus not subject to RWHT.

Second issue

As the majority determined payments did not comprise of any royalty, this meant that Justice Moshinsky’s decision in the first instance that DPT could not apply (due to royalty issue taking priority) was incorrect. Accordingly, the FFC needed to consider the application of Part IVA.

The majority found that there was no postulate that was a reasonable alternative to the scheme (i.e. entering into EBAs on terms without a royalty component), as:

- Much of the Commissioner’s position and the opinions expressed by the expert witnesses called upon by both the Commissioner and PepsiCo were based on the assumption that payments for the concentrate included a component for royalties. However, there was no evidence (as concluded in the first issue) supporting the assumption that there was a royalty.

- Notwithstanding the IP was quantified and the parties were independent, there were no inquiries or analysis into the economic substance of the arrangement and the benefits to PepsiCo / SVC. At paragraph 51, the Judges stated that:

In this case, the Commissioner’s scheme case begs the question of why the concentrate price should be understood as including a royalty. Establishing that the licence of the intellectual property was valuable is only half of the necessary inquiry. The missing other half involves the concentrate price and all of the other burdens and benefits flowing from the EBAs.

On the basis that the payment for concentrate did consist of an embedded royalty, Justice Colvin concluded a tax benefit was obtained from entering into the EBAs, where a reasonable alternative postulate was for the royalty to be paid to PepsiCo/SVC as the owners IPs instead of the nominee.

How SW can help

Our experts can assist with assessing and advising how this ongoing tax case may affect your existing and prospective cross-border arrangements and proactively engage with the ATO to deal with potential disputes.

Reach out to your SW advisor for support from our Corporate Tax team.