Australian Parliament passes mandatory climate reporting legislation

13/09/2024

Both houses of the Australian Parliament have now passed mandatory climate reporting legislation, with a new bill that will require large companies to prepare annual sustainability reports. With the aim to enhance the transparency and comparability of climate-related information.

Introduction

To enhance the transparency and accountability of climate-related matters, on 9 September 2024, the Australian Parliament passed Treasury Laws Amendment (Financial Market Infrastructure and Other Measures) Bill 2024.

This highly anticipated bill mandates that large entities adhere to the new sustainability reporting standards issued by the AASB, which align with international standards. The first group of entities will be required to submit their sustainability reports from annual reporting periods beginning 1 January 2025, with smaller entities being phased in over the following years.

New reporting requirements

A new sustainability reporting requirement has been introduced for disclosing information on climate-related matters. When applicable, the sustainability report must be prepared alongside the annual report. This report will adhere to sustainability reporting standards issued by the Australian Accounting Standards Board, which are closely aligned with international standards.

This alignment will ensure much-needed comparability across companies. The Australian equivalent standards propose making climate reporting mandatory, while other sustainability topics, such as biodiversity and human capital, remain optional.

Additionally, the final bill mandates further scenario analysis based on feedback from Parliament. Entities must disclose scenario analysis using at least both of the following scenarios:

- Low warming scenario: global average temperature increase is limited to no more than 1.5 degrees and

- High warming scenario: global average temperature increase exceeds 2.5 degrees

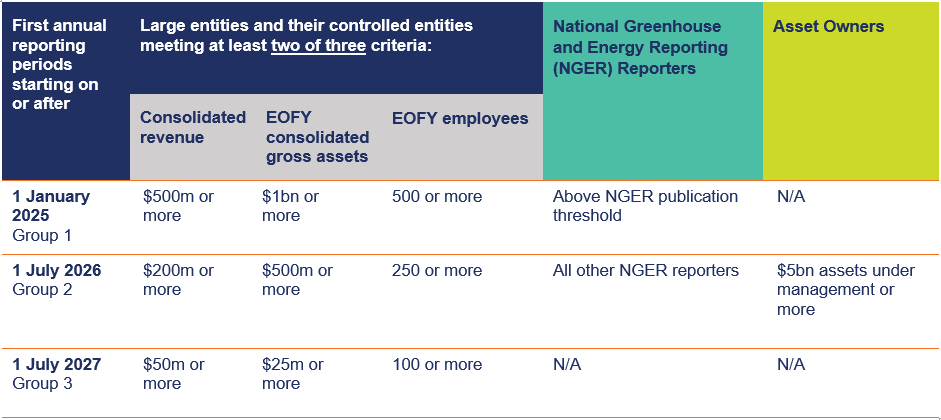

Who has to prepare annual sustainability reports and when

The government proposes a phased approach based on the size of the entities. The table below sets out the details of the threshold and date for the implementation.

The above Table is summarised from Explanatory memorandum of the bill

Group 3 entities are required to make climate disclosure if they have material risks or opportunities.

What happens to the sustainability standards?

Following the consultation feedback, the AASB has decided to revise the titles and numbering of the sustainability standards to align with IFRS S1 and S2. The new titles will be AASB S1 General Requirements for Disclosure of Sustainability-related Financial Information and AASB S2 Climate-related Disclosures. AASB S1, which covers broader sustainability topics, will be a voluntary standard, while AASB S2, focusing on climate, will be mandatory. The standards are expected to be issued in the coming weeks.

What do companies need to report?

The disclosures will need to follow the stainability standards issued by the AASB. The key areas of disclosure include:

- governance and strategies for climate-related matters

- risks and opportunities associated with climate change

- metrics and targets associated with emissions. This includes direct emissions by the company and from energy consumption (Scope 1 and 2 emissions) and emissions in the value chain (known as Scope 3 emission).

In addition to a qualitative description of the risks and opportunities, the company is also required to disclose quantitative scenario analysis. There are several reliefs proposed by the government in relation to more complex disclosure of Scope 3 emission and quantitative analysis.

The above disclosure will need to be included in a new annual sustainability report. The structure and content of the sustainability report consists:

- the climate statements for the year

- any notes to the climate statements

- any statements required by other legislative instruments to include matters concerning environmental sustainability.

- the directors’ declaration about the statements and the notes.

The annual sustainability report will be presented together with the financial report.

Audit requirements

The company’s financial auditor will audit the sustainability report. The auditing standards setter, AuASB, is currently consulting with stakeholders to determine the required level of assurance for climate-related disclosures.

Based on the most recent exposure draft, we understand the proposed audit requirement will also be phased in. We expect that in the first year of reporting, different content will be subject to different assurance requirements as below:

- limited assurance over scope 1 and 2 emissions for the first year and moving to reasonable assurance thereafter

- Other area’s disclosures will be gradually subject to review or audit from the second year onwards.

What are the next steps?

- Start preparing now!

- Familiarise yourself with the content of the proposed standards and how it affects you

- Perform a gap analysis to identify data/capability requirements

- reach out to your SW contact to help you get started

How SW can help

We can conduct gap analysis and prepare a road map to guide you on your journey.

Our team of audit and advisory experts are fully informed of the requirements of the sustainability accounting standards and can assist with providing guidance for your business, as well as keeping you abreast of developments from an Australian reporting context.

Keep an eye out for further alerts from us in respect of the finalisation of the sustainability standards by the AASB which is expected in the next few weeks, the sustainability reporting assurance standard under development by the AuASB and any announcements from ASIC on this new area.