Fringe Benefits Tax: 2020 update

20/05/2020

There have not been significant Fringe Benefit Tax (FBT) changes this year. However, the ATO have made announcements that may impact car parking benefits, FBT calculations and FBT on home to work travel by ride sharing vehicles (now considered taxi travel).

To assist with preparing the FBT calculations we have included key rates and references to tax determinations that apply to the 2020 FBT year.

Do not forget to consider your FY21 FBT liability and the impact COVID-19 may have had and may continue to have on your business. For example, some organisations may experience a significant reduction in entertainment or car parking in the current year and seek to reduce instalments as appropriate.

Key dates

In response to the COVID-19 crisis, the Government announced extensions to both the due date for lodgement of the 2020 FBT Returns and associated tax payment for all taxpayers (both self-preparers and through tax agents) to 25 June 2020.

This provides an additional month for self-preparers to lodge and an additional month for all taxpayers to settle their FBT liabilities.

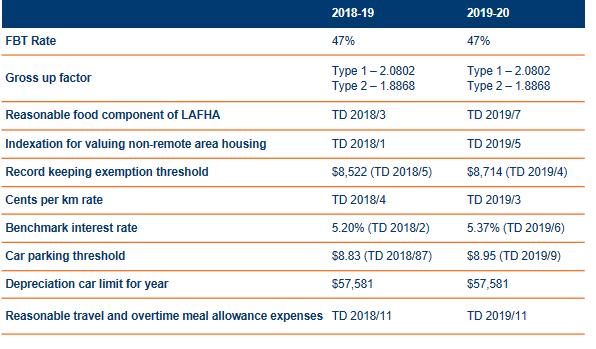

Rates and references to key tax determinations

Key Changes

Car parking valuations

The ATO has announced that it is intending to contact businesses to ensure car parking values have been calculated correctly.

Who will this impact?

Businesses that may be impacted and can expect to be contacted are those that:

- provide car parking benefits to their employees

- use the market value method.

What should you do if you believe that the value provided is too low?

There is currently no suggestion from ATO that taxpayers should obtain a second valuation to test the first valuation, however you should ensure that the market value report contains the following:

- the date of the valuation

- a precise description of the location of the car parking facilities

- the number of spaces valued

- the value of the car parking spaces based on a daily rate

- the person valuing’s name, qualifications, and signature

- declaration that the person valuing is acting at arm’s length.

Car parking tax ruling

The ATO have now withdrawn Taxation Ruling TR 96/26 and replaced it with Draft Taxation Ruling TR 2019/D5

- Historic view – car parking facilities that have a primary purpose other than providing all-day parking were not commercial parking stations for Fringe Benefits Tax (FBT) purposes e.g. parking at hospitals, shopping centres and airports.

- Proposed view – these will be considered commercial parking stations for FBT purposes.

When does it apply from?

TR 2019/D5 is proposed to apply from 1 April 2021.

Taxi travel

The treasury has released an exposure draft bill on the definition of taxi for FBT purposes proposing to replace the definition of a “taxi” in the FBT Act to mean “a car used for taxi travel (other than a limousine)”.

Generally, travel between home and work (e.g. sick employee’s trip home or return from work late at night) is considered private in nature and therefore subject to FBT. However, the FBT Act provides an exemption from FBT in respect of taxi travel between employees’ home and place of work.

Who will this impact?

All employers.

Currently, this exemption for taxi travel only applies to “a motor vehicle licenced to operate as a taxi”. This makes it difficult for employers to claim the FBT exemption in relation to ride sharing providers (such as Uber).

When does it apply from?

If enacted, the changes are proposed to take effect from the date of Royal Assent.

Get in touch

| Stephen O’Flynn |

| Sam Morris |

| Helen Wicker |

| Rahul Sanghani |