Market volatility and investing for the long term

10/03/2020

The world is watching with concern of the spread of the new coronavirus. The uncertainty is being felt around the globe and it is unsettling on a human level as well as from the perspective of how markets respond.

At ShineWing Australia, it is a fundamental principle of our investment philosophy that markets are designed to handle uncertainty, processing information in real-time as it becomes available. We see this happening when markets decline sharply, as they have recently, as well as when they rise (which they had until February when they hit record highs).

Such declines can be distressing but they are also a demonstration that the market is functioning as we would expect, that is they are re-pricing in what they expect the earnings and growth prospects of companies will be going forward.

It is important to remember that during any repricing, upwards or downwards, that markets tend to overshoot on both the upside and the downside. During both bull and bear markets we always remind ourselves and our clients that it’s never as good as it looks and it’s never as bad as it seems.

Market declines can occur when investors are forced to reassess expectations for the future. The expansion of the outbreak is causing worry among governments, companies, and individuals about the impact on the global economy. Apple announced earlier this month that it expected revenue to take a hit from problems making and selling products in China.

The Government, Reserve Bank and other officials have warned of a serious slowdown to the Australian economy whilst airlines are preparing for the toll it will take on travel and tourism, having already been hit hard by the recent bushfires is bracing for a continued slowdown in tourist numbers. These are just a few examples of how the impact of the coronavirus is being assessed by financial markets, not to mention supermarkets where the run on toilet paper, hand sanitiser and kitty litter also demonstrates that people don’t deal well with uncertainty.

The market is clearly responding to new information as it becomes known, but the market is also pricing in unknowns too. As risk increases during a time of heightened uncertainty, so do the returns investors demand for bearing that risk, which pushes prices lower.

Our investing approach is based on the principle that prices are set to deliver positive future expected returns for holding risky assets and to generate these higher returns we must bear risk and volatility. It is also important to remember that our portfolio’s hold exposure to a diversified spread of Bonds which provide a buffer against the volatility of equities.

As markets have sold off investors have moved their cash into Bonds and this provides positive returns in our portfolio’s and reduces the impact of the fall in equities. We also hold cash and bonds to provide liquidity for regular income payments so that we are not forced to sell assets in falling markets.

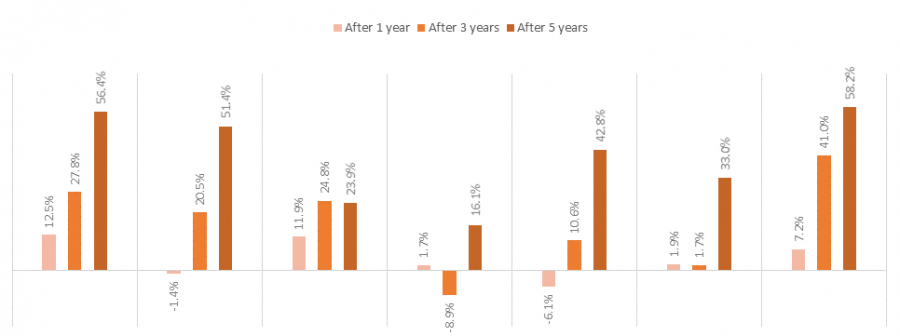

In times like these it is useful to look to the past to help guide our decisions and, if we look back at how events unfolded on a Balanced Portfolio of 60% Equities and 40% Bonds during prior market events, we can see that with the exception of the dot com crash of the early 2000’s this mix of assets produced positive returns after 3 years and all had produced very strong positive returns after 5 years.

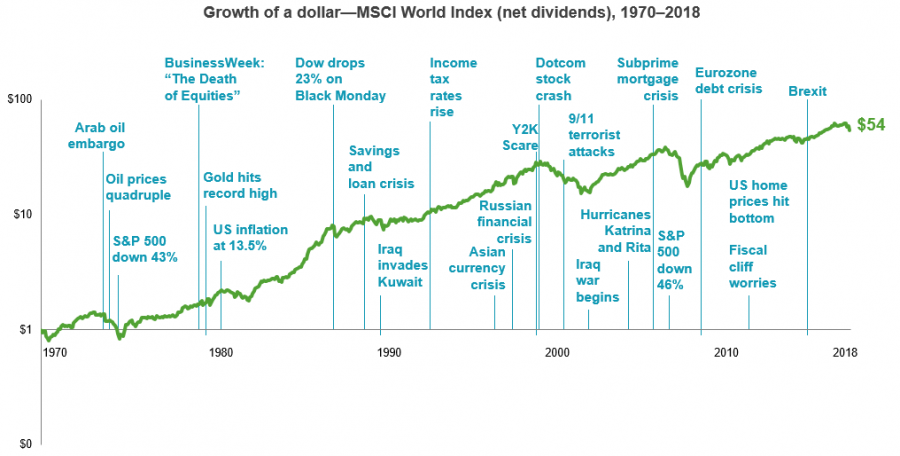

We can’t tell you when things will turn or by how much, but our expectation is that bearing today’s risk will be compensated with positive expected returns in the future. That’s been a lesson of past health crises, such as the Ebola and swine-flu outbreaks earlier this century, and of market disruptions, such as the global financial crisis of 2008–2009.

Additionally, history has shown no reliable way to identify a market peak or bottom. These beliefs argue against making market moves based on fear or speculation, even as difficult and traumatic events transpire.

Many of you have been clients for many years (including some all the way back to the 1987 market falls) but if we look back to the most recent severe downturn of 2008 you will recall that our advice then was to remain resilient, stay invested as “this too shall pass”.

Warren Buffet once famously said that “the stock market is a wonderfully efficient mechanism for transferring wealth from the impatient to the patient”. This has been shown to be true in all markets and all economic cycles where markets reward discipline and patience over the long term.

We do understand that it can be easy to feel overwhelmed by the relentless stream of news about markets. Being bombarded with data and headlines presented as impactful to your financial well-being can evoke strong emotional responses from even the most experienced investors.

When faced with short-term noise, it is easy to lose sight of the potential long-term benefits of staying invested and while we don’t have a crystal ball, remember that together we have adopted a long-term strategy so it is important to view the current market volatility and look beyond the headlines with a long term perspective.

Finally, remember that we stand side by side with you as your long term advisers. We invest in the same or similar portfolio’s to you, we have long term capital models that are based on sensible assumptions, we won’t rush to rash decisions, we provide informed advice based on data and evidence and we are focused on ensuring that you continue to meet your goals both now and into the future.

.

We continue to monitor not only the investment markets but the underlying drivers of the market movements whilst at the same time ensuring that we keep an overall long term perspective on where we have come from and where we are going. If you have any queries, concerns or just want to have a chat, be sure to get in touch with your adviser at any time.

Contacts

| Daniel Minihan |

| Matthew Baum |

| Keegan O’Rourke |