PDAs in public: When your property development arrangement gets the ATO’s attention

16/04/2026

The ATO has released Practical Compliance Guideline 2026/D2, outlining its risk framework for property development arrangements (PDAs), with a particular focus on long-term projects involving related parties and identifying what it considers high and low risk structures.

Following public consultation and the release of Taxpayer Alert TA 2026/1, which we discussed in a previous alert here, this new draft guideline focuses on PDAs where a landowner engages a related-party developer in projects spanning more than one income year.

These structures are not uncommon in the property industry and are not inherently problematic when used for commercial reasons. However, the ATO is concerned about non-arm’s length PDAs under common ownership that are designed to defer payment of tax.

Key compliance framework: green vs red risk zones

PCG 2026/D2 divides arrangements into two risk zones – green (low risk) and red (high risk) – based on the features of the deal and how income is recognised for tax purposes. The risk categorisation will determine the ATO’s level of compliance scrutiny:

Green zone (low risk)

Characterised by profit recognition during the project. Common green zone features include instances where:

- progress payments are made by the landowner to the developer as the project progresses, and the developer correspondingly returns income progressively over the project’s life

- no progress payments are made, but the developer still recognises income in stages, similar to an estimated profits basis under Taxation Ruling TR 2018/3 for long-term construction contracts

- annual land value increases are returned as income under trading stock rules, where the landowner holds the land as trading stock for tax purposes and annually includes any increase in the land’s value due to development work, in their assessable income.

Red zone (high risk)

Characterised by arrangements that artificially defer or mismatch income and deductions. Common red zone features include all the following:

- related parties and non-arm’s length terms

- use of a separate developer entity as a ‘buffer’

- timing mismatch, with deductions upfront and income deferred

- no trading stock income recognition by the landowner

- group-wide tax benefits arising from losses.

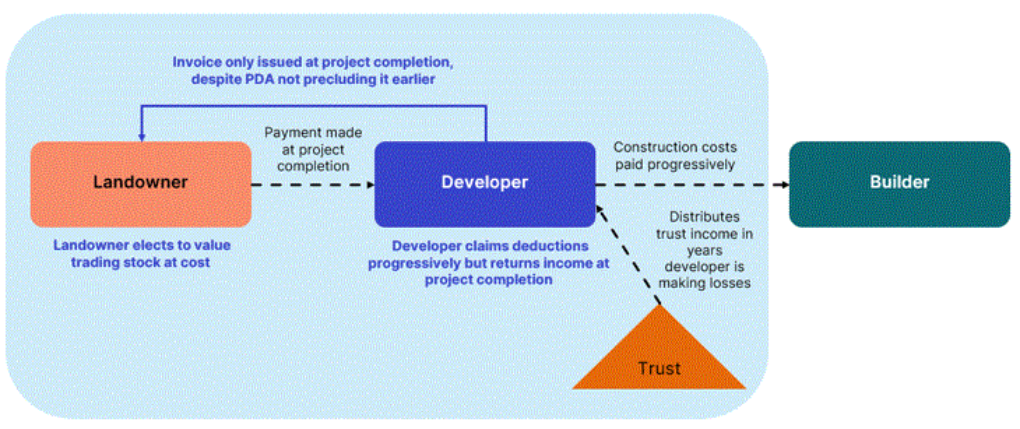

The ATO has provided several examples of high-risk structures. One such structure is shown below.

If the ATO is successful in applying Part IVA, the structure will be disregarded from an income tax perspective. From the ATO’s perspective, the key issue is the timing of income and deduction recognition, as the overall tax cost will be the same. However, if Part IVA applies and the tax benefit is denied, a taxpayer that previously reported tax losses may instead be placed in a taxable position, with interest and penalties applying.

Implications for property developers and landowners

For property developers and landowners in development projects, the Draft PCG serves as a clear warning. The ATO’s compliance radar is trained on any arrangement where profits from property development are earned collectively but taxed selectively. The key takeaways include:

Self-assess your risk profile

Taxpayers involved in property developments should immediately benchmark their arrangements against the PCG’s green and red zone criteria.

High risk of audit and Part IVA application for red zone cases

Those identified as high risk should prepare themselves for the possibility of ATO review and potential dispute.

Existing projects are not exempt

The Draft PCG will apply to both new and existing arrangements once finalised, so property groups currently using related-party development structures must not assume they are outside the scope.

Legitimate commercial arrangements remain acceptable

The ATO is careful to clarify that not all related-party development arrangements are problematic. Standard commercial practices, such as a one-off project where a landowner partners with a developer and appropriately shares project income, or where deferred payment terms are agreed but income is still accounted for each year, are generally considered not a compliance concern.

How SW can help

We are actively assisting clients in the property and construction sector to navigate the ATO’s increased focus on property development arrangements. Our team can review existing and proposed structures against the PCG’s green and red zone criteria, identify key tax and compliance risks, and provide practical recommendations to strengthen positions and align income recognition with ATO expectations.

Please contact your SW advisor to discuss how these developments may impact your arrangements and how we can support you.