Uncertain tax positions

18/10/2019

From income years commencing 1 January 2019, reporting entities will be required to recognise or account for uncertain tax positions or treatments in their financial statements.

Here are some of the key points you should be aware of:

- On first adoption, historical tax positions may need to be evaluated. At the very least, the income years open for amendment may need to be considered.

- The new requirements apply to income taxes only. They do not apply to indirect taxes, for example Goods and Services Tax or State Taxes such as stamp duties and payroll tax. Neither do they apply to employment related obligations such as employer superannuation contributions and work cover. Penalties and interests are only captured if they are accounted for as income tax expense under your accounting policies.

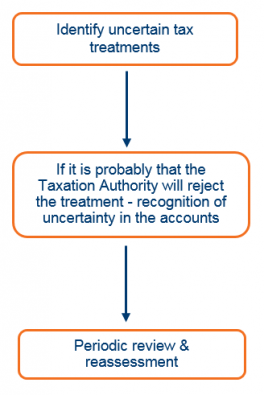

- The requirements are set out in AASB Interpretation 23 (“INT 23”) which entails a three step process as depicted below:

-

Having a reasonably arguable position may not mean that the Taxation Authority will accept the tax treatment. You may need to quantify the probability that the Taxation Authority will accept or reject your position.

-

You should consider having a conversation internally and with your auditors early to prepare for the adoption of INT 23. The questions to consider include:

-

Who determines the probability of acceptance/rejection by the Taxation Authority of the tax treatment (accept/reject probability)? Is it the finance team, the tax team or your advisors?

-

How do you deal with differences in probability assessments? Who has the final say?

-

How do we make the assessment more objective?

-

Can we apply an algorithm or formula based approach?

-

What are the relevant authorities to be considered in making the assessment?

- What is the level of documentation expected by your auditors?

-

Our Corporate and International tax team has penned a detailed article on the new requirements and presented on this topic at our 2019 Complete Tax Solutions (CTS) Conference. The article proposes a methodology to quantify the accept or reject probability which is directed towards reducing the subjectivity of the analysis.

If you would like a copy of the slide deck and article, please contact marketing@sw-au.com

Get in touch

Our experts can assist with further information.

|

Tim Hogan-Doran |